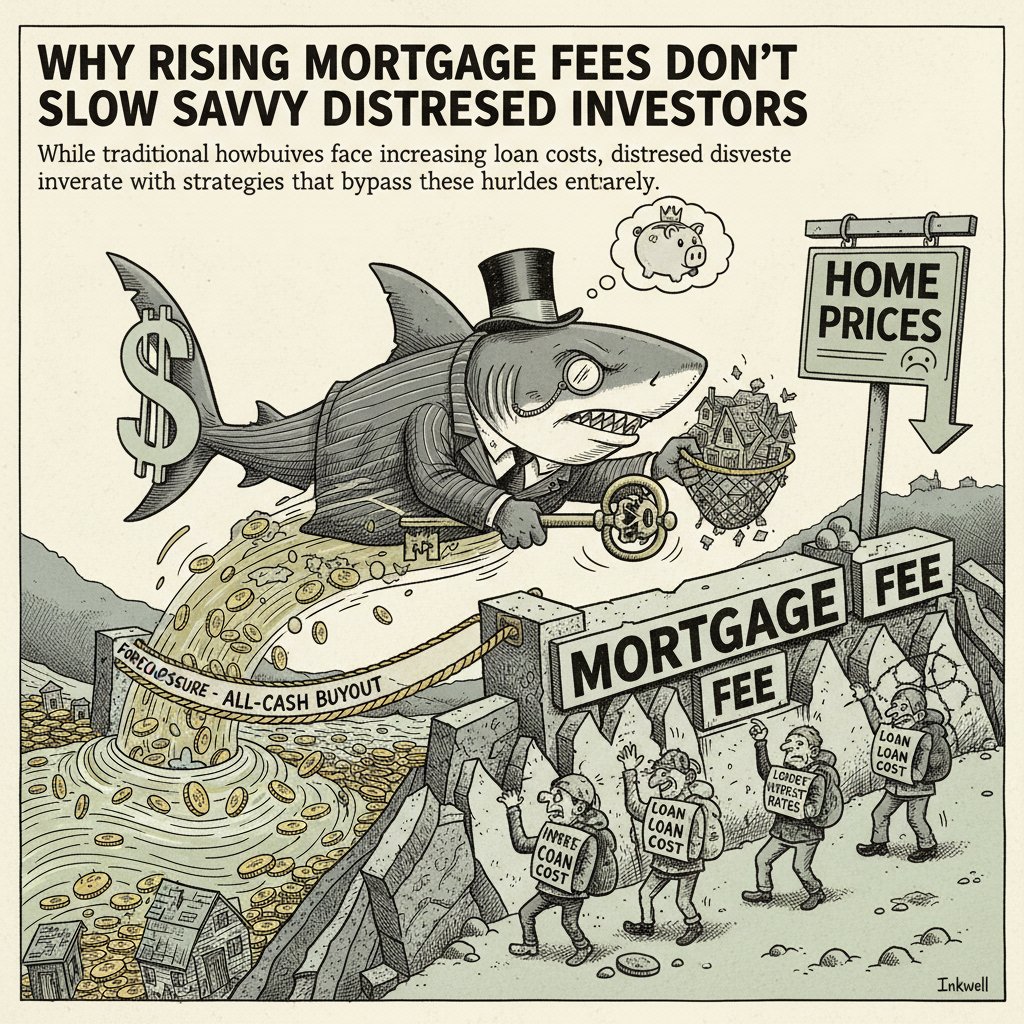

The conversation around mortgage rates often centers on affordability for owner-occupants. But for distressed real estate investors, rising rates aren't a barrier; they're a catalyst for opportunity. As rates climb, the cost of homeownership increases, pushing more marginal buyers out of the market and making it harder for homeowners to refinance out of trouble. This directly fuels the distressed inventory pipeline.

Consider the homeowner who bought at peak prices with an adjustable-rate mortgage. When their rate adjusts upward, their payment can become unsustainable. Similarly, those with interest-only loans or balloon payments face a reckoning. These are the situations that lead to pre-foreclosures, short sales, and eventually, bank-owned properties. As 'Mortgage Market Analyst' Sarah Jenkins recently noted, "Every percentage point increase in rates creates a ripple effect, eventually leading to a measurable uptick in properties entering the foreclosure process within 12-18 months."

Your strategy for 2026 shouldn't be about securing the lowest *personal* mortgage rate, but about understanding how broader rate movements impact the *sellers* you'll be working with. Focus on identifying these financially strained homeowners early. The Wilder Blueprint's Charlie 6 framework, for instance, allows you to quickly assess a property's viability and the homeowner's position, regardless of the interest rate climate.

While traditional buyers wait for rates to drop, you should be preparing to capitalize on the increased inventory and motivated sellers that higher rates inevitably bring. The ability to offer creative solutions, often involving cash or quick closes, becomes even more valuable when traditional financing is expensive or inaccessible for struggling homeowners. Build your network, refine your acquisition skills, and be ready to provide solutions when the market needs them most.